Same Inputs. Different Conclusions. We Were Right.

Inside our contrarian thesis on Stride and how we called it correctly.

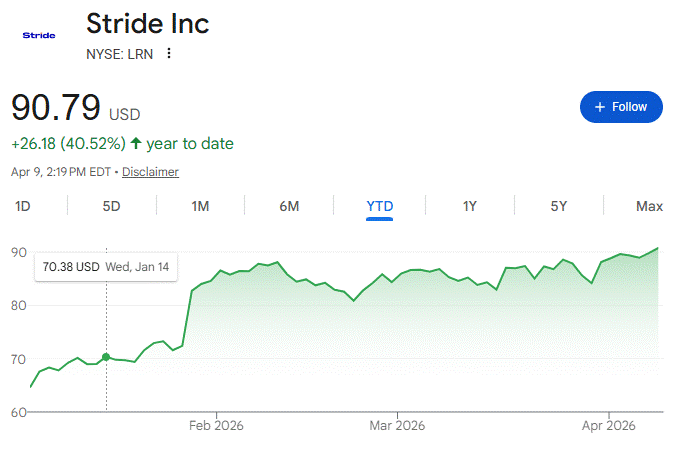

Districts criticize Stride publicly and expand their dependence on it privately. Legislators target it and then watch it migrate to a friendlier host district within the state, and preserve its revenue stream. We published a ‘better than it looks’ thesis on Stride in January at $70.38. It is trading at $90.79 today. The methodology behind that call is the same methodology we apply to every company we cover. This piece explains how we think.

Most analysis of companies and markets starts in the same place: the published record. Earnings reports, analyst coverage, industry research, expert consensus. These are real signals. They are also the signals everyone else is reading, which means by the time they shape a recommendation or a strategic plan, the insight is already priced in. The people who paid for it are not ahead. They are current, at best.

What almost nobody systematically exploits is the gap between what institutions say they will do and what they actually do under pressure. That gap is where the real intelligence lives. It is also, not coincidentally, where the most expensive strategic mistakes get made.

Exploiting that gap requires a different mental posture entirely.

Our methodology is closest to what you would get if a short seller, a business strategist, and a game theorist ran the same research process together. The short seller’s instinct: start with the assumption that the market has it wrong and build a case airtight enough to bet against the consensus. The business strategist’s discipline: understand the competitive mechanics, switching costs, and incentive structures that explain why a company’s position is stronger or weaker than it appears. The game theorist’s lens: model how the actual players, customers, regulators, boards, competitors, behave under constraint, not how they say they will behave. We start with a mass of raw material and let the misjudgment surface from the data. When the evidence consistently points toward a company being better or worse than the market believes, we become a bloodhound. We go find every structural mechanism that explains the gap, and we don’t stop until the argument has no exits.

The public company research is how we prove the methodology works. The timestamps and valuations are verifiable. The same approach works for privately-held companies too.

Buying for a large group? Ping us for Group and Enterprise Access subscriptions.

Two examples from the past three months illustrate what this produces in practice:

‘Better Than it Looks’

On January 14, we published a thesis on virtual schools operator Stride, Inc. (NYSE: LRN) in our K-12 Executive Intelligence newsletter. The stock was trading at $70.38. It had been hammered, down roughly 60% over the prior months following a complaint from a New Mexico school district and weak guidance on its October earnings call. The conventional read was straightforward: virtual schools are politically toxic, Stride is always one legislative session from collapse, and the latest controversy was just more of the same.

Our read was different. We went through every instance where a customer had signaled they may remove Stride, and tracked what happened next. This included contract termination records, board minutes, state performance audits, litigation filings, and earnings disclosures going back over a decade, alongside interviews with people who had operated inside and alongside Stride across multiple states. What that body of evidence showed, consistently across states with entirely different political climates, was that institutions almost never actually unwind from Stride when they say they will. The operational cost of disentanglement, including student records, IEP compliance, staffing models, and reporting obligations, is higher than the political cost of tolerating controversy. Districts posture publicly and expand dependence privately. That is not an inference. It is what the behavior shows, repeatedly and across jurisdictions. We also documented a specific maneuver Stride executes when a host district turns hostile: it migrates the student census, teachers, and curriculum to a new host within the same state, preserving the revenue stream while the original relationship dissolves. Indiana and New Mexico both produced documented examples of this in 2025 alone.

The market was pricing Stride based on customer rhetoric. We priced it on actual customer behavior.

As of today, Stride is trading at $90.79, up more than 40% from where it was when we published. The S&P 500 is down 1.47% in the same period.

‘Worse Than it Looks’

On January 21, we published a thesis on workforce training provider Skillsoft (NYSE: SKIL) in our Workforce Training Executive Intelligence newsletter. The stock was trading at $8.81. Our argument was that Skillsoft’s apparent stability, with retention rates reported near 99% among large enterprise customers, was masking structural decay that was invisible to buyers but visible to someone looking closely at how the product was actually used, how the capital structure constrained every strategic option.

The most useful data point is often what people say about a company once they no longer work there.

The forensic case built itself. Skillsoft was carrying approximately $558 million in long-term debt, with interest expenses consuming roughly 11% of revenue and stripping capital from R&D. Its Global Knowledge acquisition, the one supposed to add instructor-led training capability, had become a financial anchor, with revenue down nearly 18% year over year. Deferred revenue had collapsed 30% in the first nine months of FY2026, a leading indicator in SaaS economics that future bookings are contracting faster than recognized revenue. Former executives described the integration as a “Frankenstein company” that was never truly stitched together, with contradictory activity systems paralyzing the sales force and a mid-market deliberately neglected to protect margins for the Fortune 1000 accounts the debt covenants required them to defend. The AI turnaround narrative management was selling to investors was being funded by the same R&D budget it was supposedly filling.

The 99% retention headline looked like a fortress from the outside, but the structure underneath it looked like a company in managed decline, optimizing for covenant compliance at the direct expense of the product investment required to stay competitive.

As of today, Skillsoft is trading at $4.20, down more than 50% from where it was when we published. The S&P 500 is down 0.79% over the same period.

Time-Stamped Receipts:

The thesis in both cases was the same: read the behavior, not the narrative. In Stride’s case, the narrative said fragile; the behavior said embedded. In Skillsoft’s case, the headline metrics said stable; the structure said melting.

This is what we do at The Intelligence Council. We find the gap between the narrative and the reality, we build the case for why the gap exists, and we don’t stop until the argument has no exits. The public company work is how we prove it.

The timestamps don’t lie.

The Skillsoft and Stride research are both publicly available and linked above. The timestamps are there. I am making zero claims that we moved the market. I am making a claim about what we saw, and that nobody else was saying it publicly at the time.

If you want this kind of intelligence working for you, reach out. Your competitors are not standing still. director@intelligencecouncil.com

About The Intelligence Council

The Intelligence Council is an independent B2B media and executive intelligence company publishing decision-grade research for senior executives navigating complex, high-stakes markets. Our verticals cover education, AI, software, advanced manufacturing, financial services, and other sectors. Publications are built for a specialist operator audience rather than a general readership. Our flagship research, often co-produced with Emerging Strategy, combines forensic financial analysis, primary interviews, and structural analysis of how institutions actually behave under pressure. We are editorially independent and built around a single standard: intelligence that changes how leaders see a market, not content that confirms what they already believe.

About Adil Husain

Adil Husain is the Founder and Editor-in-Chief of The Intelligence Council and Managing Director of Emerging Strategy, a global strategic advisory firm. He has spent more than two decades working at the intersection of competitive strategy and international growth, including a decade based in Shanghai, and significant time on the ground in other emerging markets in Asia and Latin America. His work focuses on how institutions, markets, and competitors actually behave under constraint, and what that reveals. He writes The Husain Signal, where he publishes analysis and commentary on strategy, markets, and the intelligence business.